Mel

Haas

Mel

Haas

Home

History Finances Health

Accounts (Password Protected Pages)

Financial

Planning

We live comfortably now because we were extraordinarily lucky in the circumstances into which we were born, and by following some basic principles of financial planning. We live within our means, borrowed only through a mortgage for our home, and saved the maximum we could through our employer's savings plans. No cruises, no exotic vacations, no timeshares or second home, no car loans or leases, and houses that minimally fit our needs.

Our savings are invested very conservatively in mutual funds held by the country's largest, most reputable investment banks: Vanguard and TIAA. We have watched too many friends and relatives ruined by investing foolishly through crooked organizations like Wells Fargo and Merrill Lynch. Or worse, trying to self-manage their own portfolio. I have no talent for managing the day-to-day requirements of property, people, or investments, so I do not fiddle over the short term. The investment allocations in our funds have remained constant for many years, and I see no reason to change them.

The bulk of our savings are in Vanguard mutual funds. Most are invested in their largest index funds (i.e., funds that hold stocks and bonds chosen by following the decisions of a vast number of investors). We began with a balanced portfolio and investment strategy that consisted of half stocks and half bonds. The concept was: that when stocks go down, bonds go up.

That strategy became unreasonable when the federal government bailed out the corrupt banks in the 2008 Great Recession. Bonds, CDs, TIPs, and savings accounts stopped having returns that exceeded inflation. Firms and government entities can borrow all they need from the federal government at almost zero interest rates. Long-term corporate, municipal, and government bonds are now the equivalent of stashing money in your mattress. The value goes down over time due to inflation.

The stock market recovered well, and the stock part of our investments now far exceeds the bond part (now almost 80% stock, 20% bonds). Withdrawal from the funds for our living is still 50/50 (we have no job, so no money is being deposited into the funds).

The COVID-19/Trump disaster hit our savings 5%. We can weather that as we did with Bush's failure in 2008. We continue to live comfortably within our means and do not draw down our capital.

Retirement Planning

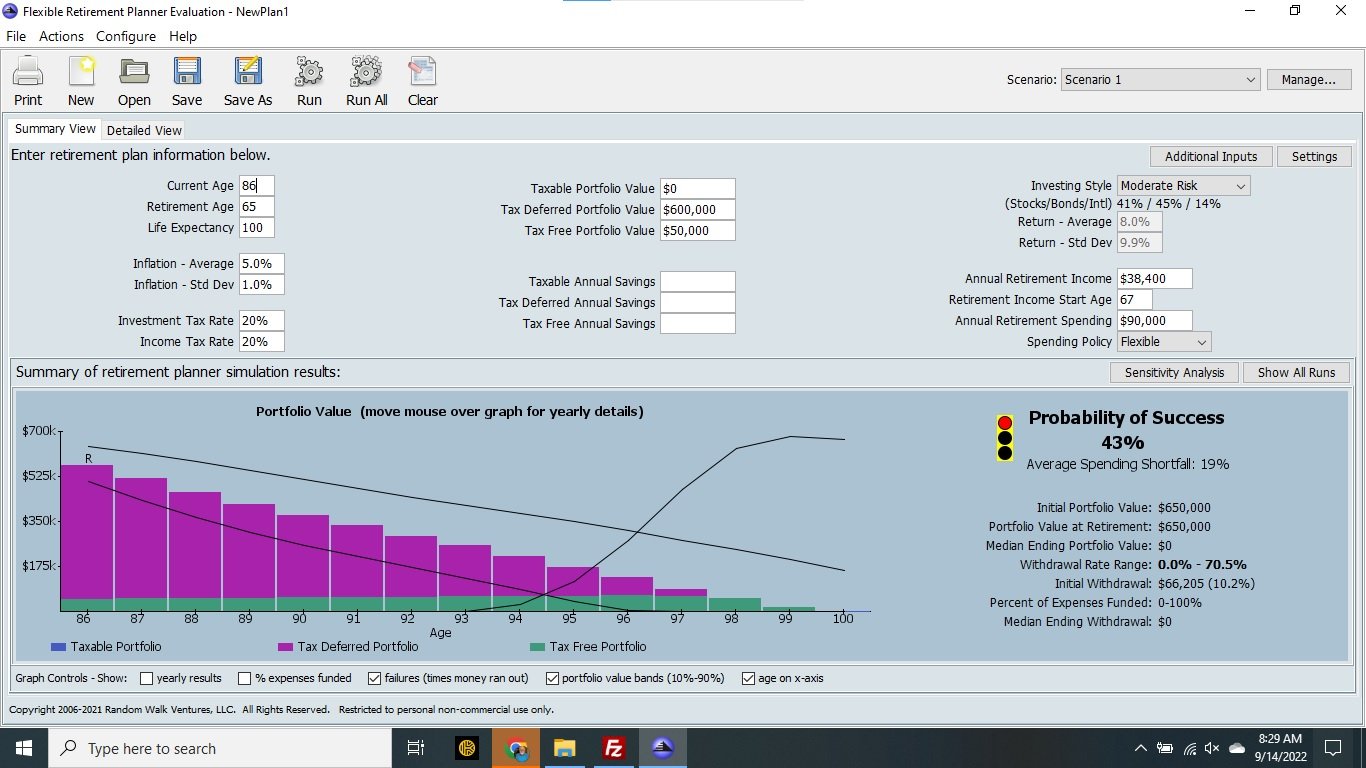

Here is a user-friendly, free graphical retirement planner that predicts how well your savings may last into the future. Download the program to your PC by just tapping DONE. You do not need/want to buy it. Plugin numbers in the white spaces that approximate your situation and guesses. You do not need to be precise. You can get most of the numbers from your current Federal Tax return.

Press RUN to present the new statistical estimate of the future. All the runs are done on your PC. Nothing goes out on the network. This is a highly regarded professional program. Here are the User Input Instructions and User Forum.

Our

Future

We

are quite comfortable here now and well able to afford to live a long time. I

discuss various situations that are expected in the future in the Heath section

of this site.

Alexa

There are many Alexa Echo units throughout the house. You can call out, "Alexa announce dinner" or "Alexa set a timer for 23 minutes" or "Alexa play my music on the everywhere group" from anywhere.

lwbook

The web site melhaas.lwbook.net is the external scrapbook of me.

The lwbook.net web site is a remnant of my failed attempt to have a Leisure World group for seniors to do projects on the Raspberry Pi. I set it up as a book club on the LW Book Network, a manually run group of book groups here. I set up a Hostinger Linux account to introduce the Raspberry Pi and interfaces to the web. I used the LW Book Club as an example of Linux, Apache, MySQL, Php/Perl/Python (LAMP) also on the Pi. The site costs almost nothing and is reliable and full featured, so I bought several years' worth of service. There are four domains on the site with SSL certificates: lwbook.net , haas.lwbook.net, melhaas.lwbook.net, mel.lwbook.net. The melhaas web domain has passwords to keep the riffraff out.

Other areas: home, history, health, music, search

Comments? Observations? Complaints? Additions?

3/26/2025 1:20 PM